1 To Watch

The cost of control: Amman risks the stability it aims to protect

Crackdowns on political opposition and public dissent are increasing the risk of instability in Jordan

May 22, 2025

Despite the timing of recent Iranian naval drills, the drivers of the US-Iran confrontation remain unchanged, with oil being secondary in the dispute.

The world is closely watching the outcome of today’s indirect US-Iran talks in Geneva, which come amid explicit decision deadlines in Washington and sustained military signalling from both sides. The USS Gerald R. Ford (CVN-78) – the world’s largest aircraft carrier – is en route to the Middle East, while the US Embassy in Beirut has ordered the evacuation of non-essential personnel, moves that indicate escalation is being treated as a viable policy option alongside diplomacy.

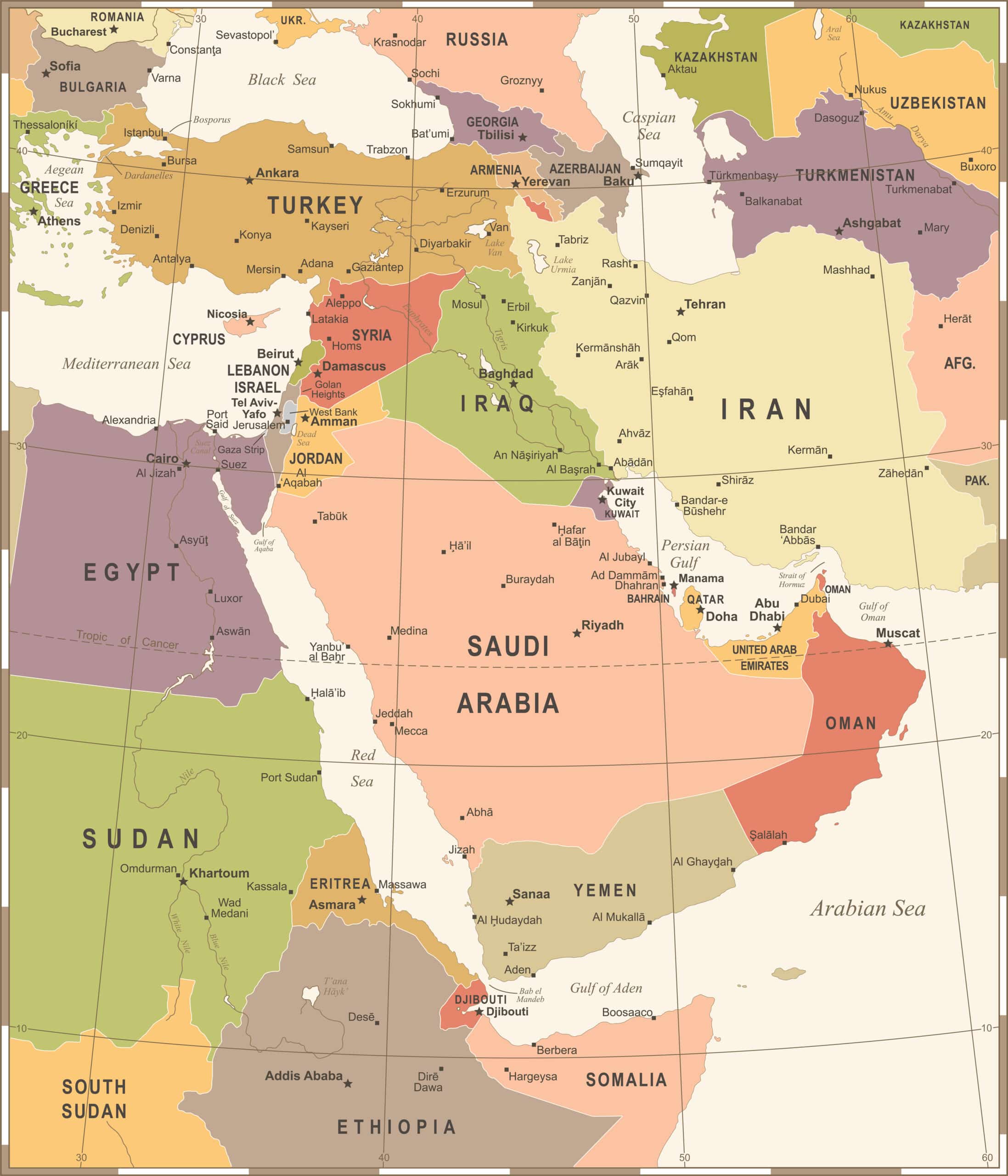

Against this backdrop of diplomacy and deterrence, Iran has also demonstrated its capacity to exert pressure. On 19 and 20 February 2026, Iran’s Islamic Revolutionary Guard Corps (IRGC) conducted live-fire naval exercises in the Strait of Hormuz, temporarily restricting vessel movements in parts of the waterway. The drills followed the earlier round of indirect US-Iran talks in Geneva on 17 February 2026. The sequencing has refocused attention on the vulnerability of a corridor through which approximately 20 million barrels per day of crude and condensate transit, equivalent to around 20 per cent of global oil consumption, according to the US Energy Information Administration. In addition, roughly 20 per cent of global liquefied natural gas trade – close to 90 billion cubic metres annually, predominantly from Qatar – passes through the Strait.

Despite their timing, the drills leave the underlying drivers of the US-Iran confrontation unchanged – Iran’s nuclear programme, ballistic missile development and regional proxy networks. Oil remains secondary in the dispute.

The principal economic risk associated with heightened tensions is disruption to shipping through the Strait of Hormuz. Even a short interruption would likely trigger a rapid increase in oil and LNG prices due to uncertainty and risk re-pricing. Recent regional escalations have demonstrated that benchmark crude can rise by around 10 per cent during periods of acute tension before retreating once flows normalise. The duration and intensity of any disruption would therefore be decisive.

Tehran’s primary objective in the energy domain remains sanctions relief to enable production and exports to return towards pre-2018 levels of roughly 2.5mbpd. The reintroduction of even 1 million barrels per day of Iranian crude would add supply to a market that is currently well balanced.

In Washington, oil prices carry electoral significance. With US mid-term elections approaching, lower petrol prices are politically advantageous for President Trump, both in terms of inflation management and voter sentiment. A sustained increase in crude prices would feed directly into domestic fuel costs, complicating inflation control and potentially affecting voter perceptions. At the same time, additional Iranian barrels entering the market under a sanctions-relief scenario would intensify competitive pressure on US shale producers. The US therefore faces a dual exposure to Gulf energy volatility, both as a consumer economy sensitive to price spikes and as a producer economy sensitive to oversupply.

This domestic exposure helps explain the importance Washington places on maintaining freedom of navigation through the Strait. The US and its allies retain the capability to restore maritime access quickly, limiting the likelihood of a sustained closure in the absence of broader war. However, even temporary interference would tighten prompt supply and increase freight and insurance costs, sustaining a risk premium beyond the immediate event window.

Alternative export routes provide only partial mitigation. The UAE’s Habshan-Fujairah pipeline can transport approximately 1.5 to 1.8mbpd, covering around 60% of national production capacity. Saudi Arabia’s East-West Pipeline to Yanbu has capacity of roughly 5mbpd, slightly more than half of its export volumes. These routes reduce reliance on Hormuz but impose a physical ceiling.

OPEC+ spare capacity is estimated at roughly 2mbpd and is concentrated mainly in Saudi Arabia and the UAE. In a full Strait closure scenario, however, spare capacity would be constrained by export infrastructure limits, as only volumes that can be rerouted via Red Sea or Fujairah outlets could reach the market. In partial disruption scenarios, spare capacity could still be deployed, but its effectiveness would depend on the duration and severity of the interruption.

Asian economies would be most directly exposed. China, India, Japan and South Korea import significant volumes of Gulf crude, while LNG buyers across South and East Asia depend heavily on Qatari cargoes transiting Hormuz. Europe would experience indirect effects through higher global benchmark prices and tighter LNG availability, particularly given its continued reliance on seaborne gas to offset reduced Russian pipeline flows.

A prolonged and deliberate closure of the Strait would also constrain Iran’s own exports and risk direct military retaliation. For that reason, such an outcome remains improbable outside an extreme confrontation. However, the risk environment is complicated by Iran’s network of regional partners and proxies. Attacks on tankers or energy infrastructure carried out by non-state actors – whether directed, tacitly enabled or undertaken autonomously – increase unpredictability and the potential for miscalculation. Escalatory dynamics could therefore emerge even without an explicit decision in Tehran to close the waterway.

At the inaugural Board of Peace meeting in Washington, DC, on 19 February 2026, President Trump stated that the world would know within the “next ten days [or so]” whether he intended to authorise military action against Iran. The comment sets a decision point at the end of February. A similar timeframe was signalled during the June 2025 Iran–Israel conflict, but President Trump ordered direct strikes just days into that period. The USS Gerald Ford is undergoing refuelling and essential maintenance at Souda Bay in Crete, but is likely to sail in advance of any strike.

In the near term, markets are likely to retain a contained geopolitical risk premium rather than price in sustained oil supply loss. Absent material damage to infrastructure or a prolonged interruption of shipping, volatility is likely to remain episodic. Unlike Ukraine, where sustained conflict and sanctions structurally reshaped trade flows over time, any Gulf escalation would more likely be sharp and limited in duration, particularly in the absence of ground engagement.

Progress towards sanctions relief would introduce additional Iranian supply over the medium term, exerting downward pressure on prices. Conversely, direct strikes on energy infrastructure in Saudi Arabia or the UAE, or sustained proxy activity targeting maritime traffic, would represent a materially different risk scenario, potentially keeping prices elevated depending on the scale of damage and repair timelines.

1 To Watch

Crackdowns on political opposition and public dissent are increasing the risk of instability in Jordan

May 22, 2025

1 To Watch

Donald Trump has an historic opportunity to negotiate a much tougher nuclear deal with Iran – will he seize it?

April 3, 2025

1 To Watch

The transitional government must focus on four key areas to ensure that unity is maintained.

December 24, 2024

© Azure Strategy 2026.